Fractional Reserve Banking

In the past, I've explained how inflation punishes savers, why the official figures understate the real inflation we experience, and why real estate is uniquely positioned to exploit inflation through leverage . But this begs another question. If borrowing benefits the investor, allowing us to own assets with bank's money, why would banks lend to us at all instead of buying these supposedly superior assets for themselves?

In the past, I've explained how inflation punishes savers, why the official figures understate the real inflation we experience, and why real estate is uniquely positioned to exploit inflation through leverage . But this begs another question. If borrowing benefits the investor, allowing us to own assets with bank's money, why would banks lend to us at all instead of buying these supposedly superior assets for themselves?

Banks have been in this business for over a century. They have more capital, more data, and more lawyers than any individual investor. If this is a zero-sum game, the smart money should be on the institution with vastly more resources. The bank should win every time, at your expense.

The answer is that the economy isn't zero-sum. Banks play a different game, and exploit a different mechanism, which further contributes to inflation. Just like in the game of poker, you're not playing against the house, but against other players. Understanding the game banks play is key to building wealth.

How Banks Actually Work

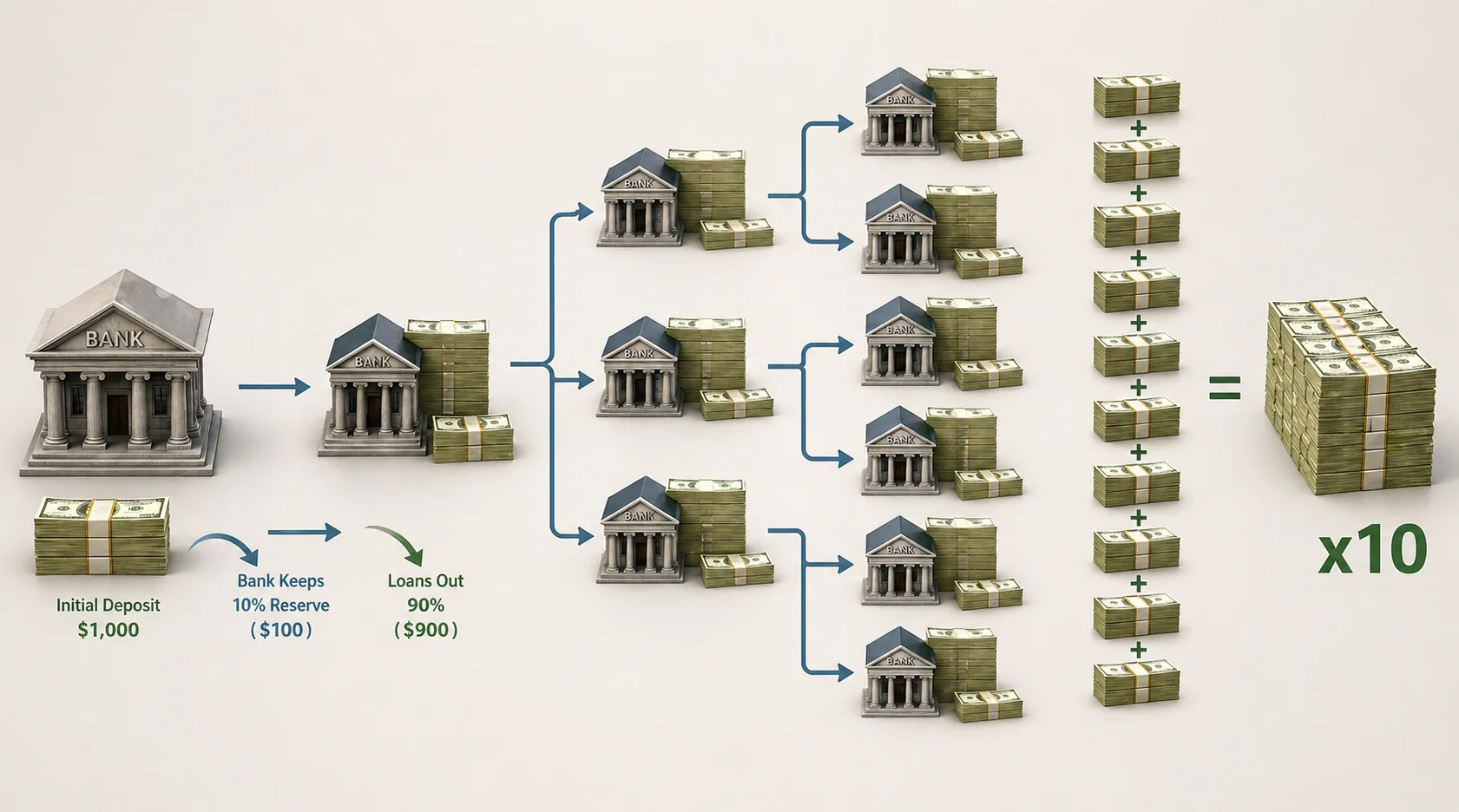

Let's say Bob deposits $1,000 at a local bank. Now the bank has money they can lend to others. Sally borrows $900 from the same bank. If Sally were to deposit that borrowed money in her bank, the banking system now has $1,900 of circulating supply. $900 materialized out of thin air. This example uses a reserve ratio of 10%, meaning that banks can only lend out 90% of the assets they own. If we were to extrapolate this example forward with more borrowers, the initial $1000 of real money would generate $9,000 of derived (borrowed) money out of thin air. Total circulating supply in this banking system would be $10,000. This total monetary supply is called broad money, which includes the original supply as well as all derivatives tied to it.

This is fractional reserve banking. The bank holds only a fraction of deposits in reserve; the rest gets lent out. Just like the investor, the bank is a landlord. But the asset that the bank rents out is depositor's money. Fractional reserve banking is a form of leverage too. But this isn't even the scary part. In 2020, the Federal Reserve reduced reserve requirements to zero. Banks are no longer legally required to hold any fraction in reserve. The multiplication has no theoretical ceiling.

When Everyone Wants Their Money Back

The system's vulnerability is obvious: it works until everyone shows up at once. This is a bank run. The Great Depression is the textbook case. Between 1930 and 1933, over 9,000 banks failed as panicked depositors rushed to withdraw simultaneously. Those banks weren't insolvent on paper. The money was there, just locked up in loans that couldn't be unwound fast enough. Silicon Valley Bank collapsed in March 2023 under the same dynamic: $42 billion in withdrawal requests arrived in a single day. SVB had invested depositor funds in long-term bonds that lost value when rates rose. When depositors demanded their money, there wasn't enough liquid to cover it. The bank was seized within 48 hours.

Congress created the Federal Reserve in 1913 specifically for this: a "lender of last resort" that backstops banks when panic outpaces reserves. It traded an acute problem for a chronic one. Bank runs went away. Inflation became the tax we all pay instead.

The Bank Plays a Different Game

When you take out a mortgage on a rental property, you and the bank are not competing for the same prize. You're playing completely different games.

The bank's bet is narrow: "Will this borrower keep making monthly payments?" That's the entire wager. Not whether the property appreciates. Not whether rents keep pace with inflation. Just: will the check arrive on time, every month, for 30 years. Banks have a century of actuarial data on default rates by credit score, loan-to-value ratio, property type, and market cycle. They structure their underwriting to keep the odds heavily in their favor. Foreclosure (actually taking the property) is their worst-case outcome. It's expensive and legally messy, and exactly what they're trying to avoid. They also make terrible landlords because they don't understand markets or property upkeep.

Your bet is different: "Will this asset appreciate, generate cash flow above my carrying costs, and deliver returns amplified by leverage that outpace inflation?" Higher variance. Higher upside. An entirely separate wager.

Banks don't lend your deposit. The Bank of England confirmed this in a 2014 paper: "When a bank makes a loan, it simultaneously creates a matching deposit in the borrower's bank account, thereby creating new money." The loan creates the deposit. The money didn't exist before the bank lent it. The Philadelphia Fed found that from 2001 to 2020, approximately 92% of all deposits in the U.S. banking system were created through lending, not through people depositing cash.

A bank with $100 million in deposits doesn't lend $90 million and keep $10 million. It uses that $100 million as a base to originate approximately $1 billion in loans through the fractional reserve process. At 6% annual interest, that's $60 million in annual interest income on $100 million of actual depositor capital. The bank doesn't need your property to appreciate. It doesn't need it to go up at all. It already captured its return the moment it created the money and put it to work. The skeptic picturing a poker table, where one player's chips come from another, is misreading the room. The bank is the casino. It's not trying to beat you at your game; it's running a completely different one.

The Borrower's Side

On the borrower's side, the math works differently but lands in the same place. As I covered in the leverage post, a 5% price increase on a property you bought with 20% down produces a 25% return on your actual invested cash. The leverage multiplies your effective return. Meanwhile, the bank earns 6% on money it fabricated through the fractional reserve process at almost no cost. Two different return profiles. Neither one at the expense of the other.

Then add the inflation component. Your $400,000 mortgage is a fixed nominal obligation. Every year, inflation erodes its real value. At 3% annual inflation, that $400,000 balance represents roughly $298,000 in today's purchasing power after a decade. Inflation has quietly contributed $102,000 toward your debt in real terms, without you writing a single extra check. Meanwhile, your asset has appreciated in nominal terms. You benefit twice: the asset goes up, and the real debt goes down. The bank holds a nominal claim that loses real value over time. This doesn't hurt them, because the FRB mechanics mean they've already deployed that capital across many loans and collected interest throughout.

This is why the wealthy love debt. Not any debt. Specifically debt backed by appreciating assets, in a system designed to expand the monetary supply. Savers get punished by inflation, borrowers harness it.

The Tailwind for Real Estate Investors

Fractional reserve banking gives real estate investors two tailwinds, both pulling in the same direction. The first is price support through money creation. Every loan a bank originates creates new money that enters the economy. Much of it flows through mortgage lending: more buyers competing for the same housing stock, which pushes prices up. When the Fed cut rates during COVID and banks flooded the market with new credit, the M2 money supply grew roughly 40% between February 2020 and February 2022. Home prices followed. Inflation hit 9.1% in June 2022, the highest in 40 years. The investors who owned real estate before the surge rode it up. The ones sitting in cash watched their purchasing power disappear.

The second is the compounding benefit of fixed nominal debt in an inflationary world. Your mortgage payment is the same nominal dollar amount in Year 1 and Year 20. But in Year 20, after two decades of inflation, that fixed payment represents a fraction of its original purchasing power. Rents, wages, groceries, utilities: all of these float upward. Your debt payment doesn't.

In 2015, I bought a Chicago property for $60,000 cash, put $30,000 into rehab, and a year later refinanced and pulled out $120,000. That's $30,000 more than I had put into the deal, while still owning the property and collecting $500/month in net rent, an infinite return. The bank fabricated that money against the property's appraised value, handed it to me, and still came out ahead on its end.

So Why Do Banks Lend to Us?

So why does a bank lend money when you're the one who's going to profit from the loan? Let's run the actual numbers on a $500,000 rental property: 20% down ($100,000), $400,000 mortgage at 6%.

The bank's position: Under traditional fractional reserve mechanics (10% reserve ratio), a $400,000 loan requires approximately $40,000 in real depositor capital as the base. Today with zero reserve requirements, the real capital base is even smaller. At 6% annual interest, Year 1 interest income is roughly $23,880. Return on the $40,000 real capital: approximately 60% annually, before subtracting deposit costs. Over 10 years with standard 30-year amortization, the bank collects roughly $218,000 in interest payments while the loan remains a performing asset on their books.

The borrower's position: The same property at 5% annual appreciation reaches approximately $814,000 after 10 years. After a decade of payments, the remaining mortgage balance is approximately $339,000. Equity at Year 10: $814,000 − $339,000 = $475,000, compared to the $100,000 initially invested. A 375% return on invested capital. Add $500/month net cash flow over 10 years (conservative for a well-purchased rental): another $60,000.

Inflation adjustment: at 3% annual inflation, the $400,000 mortgage represents roughly $298,000 in today's purchasing power after 10 years. Inflation contributed the equivalent of $102,000 in real debt reduction without an extra payment.

| Bank | Borrower | |

|---|---|---|

| Real capital deployed | ~$40K | $100K |

| 10-year gross return | ~$218K interest | ~$375K equity + $60K cash flow |

| Return on deployed capital | ~545% | ~435% |

That 5% appreciation rate is doing more work in the borrower's calculation than any other input. Here's how the same deal looks across different markets:

| Appreciation rate | Year-10 value | Equity gain | Cash flow | Total return on $100K |

|---|---|---|---|---|

| 3% (stagnant, matches inflation) | ~$672K | ~$233K | $60K | ~293% |

| 5% (typical market) | ~$814K | ~$375K | $60K | ~435% |

| 6% (cherry-picked market) | ~$895K | ~$456K | $60K | ~516% |

Notice the spread. At 3%, equity gain shrinks by $142K compared to the 5% baseline. At 6%, it grows by $81K in the other direction. Same property, same down payment, same loan, same inflation tailwind on the debt. Appreciation is the only input you can actually shop for. Cash flow is bounded by local rents. Interest rates are set by the Fed. Tax treatment is set by Congress. But which market you buy in, that one is yours to pick. Investomation Pro is the tool I built for exactly that question: which metros look positioned to appreciate faster than inflation over the next decade. $79/month, less than three coffees a week, for the same data I use on my own deals.

The government designed our economy to be permanently inflationary, which leaves you with a forced choice: stay a saver and watch 2-5% of your buying power erode every year, or become a borrower and watch 2-5% of your debt obligation erode instead. Same math, opposite direction. I used to be a saver too, until I realized I was getting punished for it. The system gives us lemons. The least I can do is make lemonade.