FTX Didn't Break Crypto

Through 2021 and 2022 I wrote a long line of posts about crypto: why it matters, the specific use cases, and the technology that makes the asset class interesting. I also covered the failures when they happened: Terra/Luna in May 2022, Harmony Network in October.

Through 2021 and 2022 I wrote a long line of posts about crypto: why it matters, the specific use cases, and the technology that makes the asset class interesting. I also covered the failures when they happened: Terra/Luna in May 2022, Harmony Network in October.

So I'm not going to skip FTX either. By the time it hit, 2022 had already been a brutal year for crypto, including for me. A lot of people I know got hit harder by the FTX wave specifically. The popular take after all this is that crypto was always a scam and the believers were rubes. That's not the right read, and I want to explain why I think so.

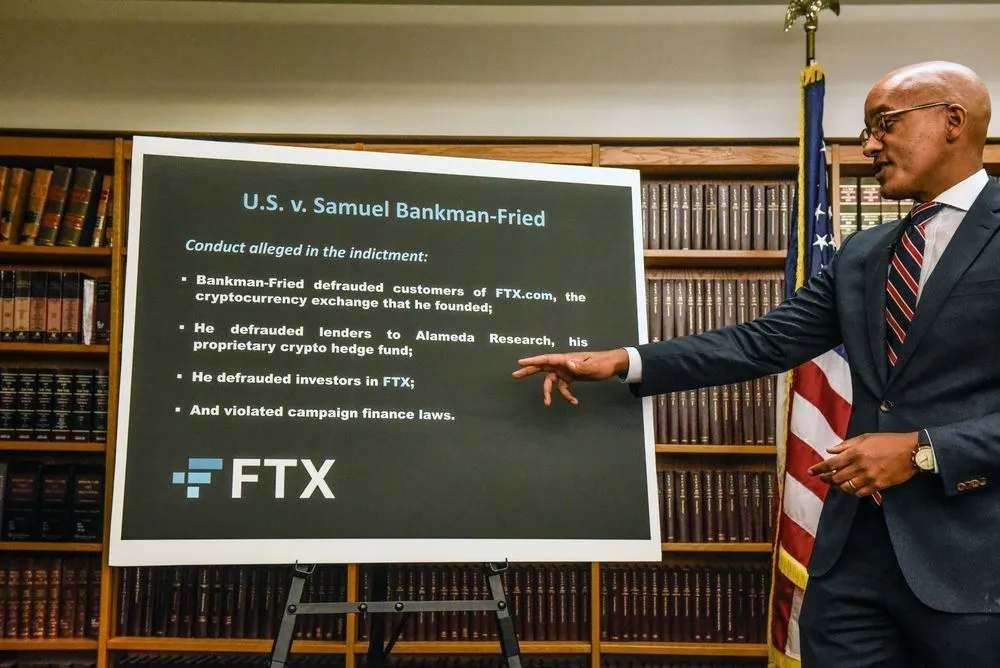

What FTX was

Strip the cryptocurrency layer off the FTX story and what you have left is a textbook financial fraud. Sam Bankman-Fried ran a centralized exchange where customers deposited assets for safekeeping. Behind the scenes, he commingled those customer deposits with his sister firm Alameda Research and used them as margin for proprietary trading bets. When the bets went wrong, the customer money was already in the wrong hands. Lehman Brothers committed the same flavor of leverage-the-customer-pool fraud in 2008. MF Global did it in 2011. Bear Stearns. Drexel Burnham. Each one was a centralized custodian abusing the trust-deposit relationship, and after each one we shrugged at the bad actor and kept using banks.

What's different about FTX in the public mind is that it happened in crypto, and crypto was the new thing that was supposed to be different. So when an FTX-shaped scandal hit, people concluded the underlying technology was the rotten part. But the technology had nothing to do with what SBF did. He could have run the same fraud at a brokerage, a bank, or a hedge fund. The fact that the chips on his balance sheet had ticker symbols like SOL and BTC instead of MSFT and SPY was incidental.

Why the obvious solutions miss the point

Two solutions get proposed every time something like this happens. The first is proof of reserves. The second is more regulation. Both miss the point.

Proof of reserves is theatrical. It only shows what an exchange chooses to show. An exchange can publish a Merkle-tree attestation that the dollars it's claiming to hold are sitting in a particular wallet, and that attestation tells you nothing about whether the wallet was funded by another exchange's customer deposits twelve hours before the snapshot. The 2022 industry tour of "proof of reserves" pages after FTX was mostly an exercise in showing each other what each exchange wanted to show. There's no way to prove what's not in reserves, only what is.

The regulation argument is louder but lands in the same place. If the goal is regulated centralized custody with deposit insurance and audit trails, that already exists. It's called banking. Crypto's original pitch was specifically that you don't have to trust a regulated counterparty with your money. Asking for regulation to make crypto exchanges as safe as banks is asking for the banks we already have, with worse tax treatment.

The actual lesson: self-custody

The lesson FTX should have taught the industry comes down to one question: who's holding your keys?

When crypto worked the way it was originally designed to work, you held your own keys and your assets sat at an address only you could spend from. Bitcoin's whole point was that you didn't need a bank, a clearinghouse, or a trusted intermediary to move money. "Not your keys, not your coins" was a slogan for a reason. Then the industry built convenient exchanges, retail piled in, and most people ended up holding their crypto at exchanges because keeping a hardware wallet safe is harder than logging into Coinbase. By 2021, most of the retail money in crypto was held by people who were one centralized counterparty failure away from losing everything.

FTX wasn't a failure of crypto. It was a failure of users who treated a crypto exchange like a bank. Holding your own keys is the price of admission for the asset class behaving the way the asset class was supposed to behave. If you're not willing to do that, an exchange is going to charge you for the privilege of holding your money, and every once in a while one of those exchanges will turn out to be Lehman Brothers in different colors.

Where I still stand

The use cases I wrote about a year before FTX collapsed don't depend on Sam Bankman-Fried. Oracles still let smart contracts read real-world data. Stablecoins still enable cross-border settlement that doesn't require a correspondent banking relationship. NFTs still represent ownership of specific digital objects, whether or not the market for any particular collection turns out to be a fad. The blockchain trilemma I wrote about still applies and still constrains protocol design. Bitcoin still has a fixed supply schedule that doesn't depend on a central bank's reading of the inflation tea leaves.

None of that changed in November 2022. What changed in November 2022 was that one exchange operator turned out to be a fraud, and the public narrative collapsed any distinction between the operator and the asset class. The two are not the same. The macro case for crypto, that programmable money and decentralized settlement are useful primitives in a world where fiat currencies are losing real value, is unchanged. The micro case for paying attention to specific use cases is unchanged.

What changed, for me, is the operational discipline. I custody my own coins where I can. I treat any exchange balance as a position I'm intentionally short on counterparty trust. I size positions accordingly. The technology and the macro case are still right. The trust assumptions a lot of us were making to make the technology convenient were not.